To the point

Have you finished your Christmas shopping? Start analyzing your personal finances for the new year!

Introduction

Three indispensable resources for personal finance

Ça coûte cher, être un adulte!

La retraite à 40 ans: comment déjouer le système pour atteindre la liberté financière?

L'argent ne dort jamais

Start 2021 with healthy finances

Managing the impact of COVID-19 on our personal finances

Eliminate your debts

Start saving early

Make a budget

Track your credit report

Stay informed about finances

Conclusion

Let’s talk about something that everyone has to deal with. Personal finances. Let’s face it, there’s no shortage of expenses in life! And to make sure we’re aware of what’s going on, it’s important to analyze what goes into our pockets as well as what comes out of them.

Introduction

Ever since we were young, we’ve been surrounded by finances. With a distracted gaze, as children we were already looking at how our parents spent their money to buy us a magazine or candy.

Over time, you start earning money yourself. Some of us quickly took responsibility, having received an amount each week that we put away in the bank or set aside. Others spent the money as quickly as they earned it.

Most of us didn’t start taking finances seriously until we were in our 30s. thirties due to the pace of life:friends, career, renting, traveling instead of thinking about saving or investing money in our twenties!

Many people have been keeping a close eye on their finances for a long time, like our friend Frédéric, an Excel spreadsheet pro! But others may be like me and are still trying to understand the ropes of this world and to avoid making mistakes.

And how do we teach our children to understand what finances are all about? That’s where I got the idea to share with you some tools (books and blogs) that we have discovered over the last few years, as well as to give you some advice on how to spend your money better, and be able to live easily according to your desires and dreams.

Three indispensable resources for personal finance

1 - The book by Béatrice Bernard Poulin - Ça coûte cher, être un adulte!

To begin with, have you ever once made a list of your expense items? How do you sort it out, what are your tricks? Do you shop around for the best prices? Do you negotiate your insurance contracts and other subscriptions? How do we know we’re not paying at the top of the price range? Are they necessary expenses?

Between our first outing to a restaurant or bar, our first car, our first grocery store, our first job, our first apartment, our first trip, our first trip around the world, etc. Phew… where’s the guide? We are all looking for tricks to guide us, in books, in articles… Otherwise we wouldn’t be sharing tips every day, like in our Facebook group!

Blogger Béatrice Bernard-Poulin addresses ALL of these questions with her book “Ça coûte CHER, être un ADULTE !”.

This title is very appealing to me. Whether you are an adult or a teenager, you face great challenges. We all face the cost of living and must make the right choices in order to save money and have fun!

No universal courses are offered once you’re out of school. We have to make do with what we know and what our parents teach us. And we all agree that we all have a different financial education.

A minimum of judgment is essential to compare, untangle contracts, negotiate, organize. I’ve learned on the spot, like everyone else, and I’ve made mistakes, like everyone else. I would have liked to be told sometimes “You should choose this because…” or “Do you know that this kind of help exists?”

In her book, Beatrice popularizes and reviews savings, compound interest, debts before giving us tips on our first job, first expenses, first budget, on the insurance to take or on the art of negotiation, etc..

She is like a coach who pushes us to question ourselves, to review our objectives. A gold mine for any young person who wants to become autonomous quickly.

Beatrice’s book should be put in the hands of your kids once they become young adults! A guide to which they can refer according to each phase of their life and when some of them want to advocate for their autonomy rather than ask their parents for help.

Her book “Ça coûte CHER, être un ADULTE!” is available in all bookstores or online and is already a favourite! Online, you’ll find it everywhere like on Renaud Brayor bookshops.ca.

Beatrice’s blog is also to be discovered since she talks about her favourites, about travel, she gives ideas for holiday activities or how to make an assessment of your year. She also offers financial tools to simplify your life and an organization program, L’année qui compte. She even organizes conferences and puts videos on YouTube.

2 - Jean-Sébastien Pilotte's book - La retraite à 40 ans: comment déjouer le système pour atteindre la liberté financière?

Want to go further? Making a budget and sticking to it is a first step towards financial independence.

According to Jean-Sébastien Pilotte, frugalist author of “La retraite à 40 ans: comment déjouer le système pour atteindre la liberté financière“, financial freedom is within everyone’s reach!

Anyone can access it with the right choices and create a “freedom fund” to be financially free, thanks to intensive savings!

While traveling with his wife, Jean-Sébastien realized that “the standard of living of an average Quebecer is an ideal to be reached for the vast majority of the inhabitants of this planet”. Happiness is not found in money.

Founder of a blog called jeuneretraite.ca, his ambition was to take early retirement and show the way for everyone to be frugal.

In his book “La retraite à 40 ans: comment déjouer le système pour atteindre la liberté financière“, he reveals everything: his project, his objectives and his strategy so that we can all become our own CEO.

You will be able to calculate your net worth and put a price on your freedom; understand the FIRE concept, or the concept of underconsumption. Finally how to hack your budget, invest in the stock market or get rich, thanks to children.

Jean-Sébastien has even started to collect reward program and credit card points by “religiously” following milesopedia’s strategies!

Is it already too late for us? No! We can still make the choices that will lead us to earlier retirement. And as for our children, it is good to teach them early on the value of things, to find happiness and freedom without being tied to money so that our children can be their own “master” one day.

His book is also available in all bookstores and online at Renault Bray or Libraires.ca.

Jean-Sébastien maintains a fascinating blog, Jeune retraité, where you can find stories of experiences, statistics and these good frugal tricks.

3 - Youcef Ghellache's Facebook group - L'argent ne dort jamais

Before discovering Beatrice and Jean-Sébastien, Youcef was the one who opened the way to personal finance for us, a few years ago!

Youcef Ghellache is a teacher in life and has developed tools to help Quebecers regain control of their finances.

To help us do this, he founded the Facebook group “L’argent ne dort jamais”, a community that keeps growing too.

In 2020, he launched a complete training available online at Educfinance with several course modules to provide you with an important support in your financial decisions.

You can trust him and the team around him, and ask them all your questions about this great group, or follow the YouTube channel.

Start 2021 with healthy finances

1 - Managing the impact of COVID-19 on our personal finances

Budgets have been a challenge for everyone this year!

The COVID-19 crisis has unfortunately spared no one. Jobs lost, lives changed, everyone was affected in some way.

The federal government has offered solutions to address the impact of this crisis and to help citizens and businesses hold on, such as the Canada Emergency Response Benefit (CERB), Canada Emergency Wage Subsidy (CEWS), the Canada Recovery Sickness Benefit (CRSB) and many others.

Some bring their share of benefits as well as drawbacks if one mismanages their affairs. So be sure to keep track of your business. It will be important to report amounts received from the CERB, for example, on your tax return.

2 - Eliminate your debts

Our community is wise, as we recommend that everyone get into the business of using credit cards as long as you pay attention to your finances and never accumulate debt or pay interest as we have said many times.

But there are still consumers who don’t pay attention. Rule number 1 when you have a credit card: don’t leave any balance on them!

So if you have a debt:

- make an appointment with your bank’s financial advisor,read the two books recommended above and join the Youcef’s community!

- put a plan in place to work towards eliminating your debt over time!

- learn about the advantages of your credit card and compare it with other credit cards on milesopedia: some cards can help you eliminate your debt, provided, once again, that you do it right.

3 - Start saving early

I come back to what I was saying earlier, but it is important to get into the habit of putting money aside early. Starting to save early can be beneficial for unexpected events that can happen at any age in life. Saving for school, children, retirement. All types of savings exist. Ask yourself the right questions and how much you could set aside.

An example from Beatrice’s book struck me: the purchase of a $50 sweater. Who hasn’t bought a piece of clothing on a whim and then only wore it on once or twice? Beatrice gives a tip to calculate the “real cost” of a garment, i.e. the number of working hours needed to buy it.

If you wear the $50 sweater fifty times, it’s $1.00 a pop… And if you only wear the $10 sweater once because you don’t really like it, it means it cost you $10 a pop!

Béatrice Bernard-Poulin

The money from that $10 sweater could have gone into a savings account.

Think about your expenses and plan your savings strategy, set goals, create a diversified investment portfolio (especially since there are easy tools such as Wealthsimple): in short, make sure you have your back before spending your entire budget on a whim.

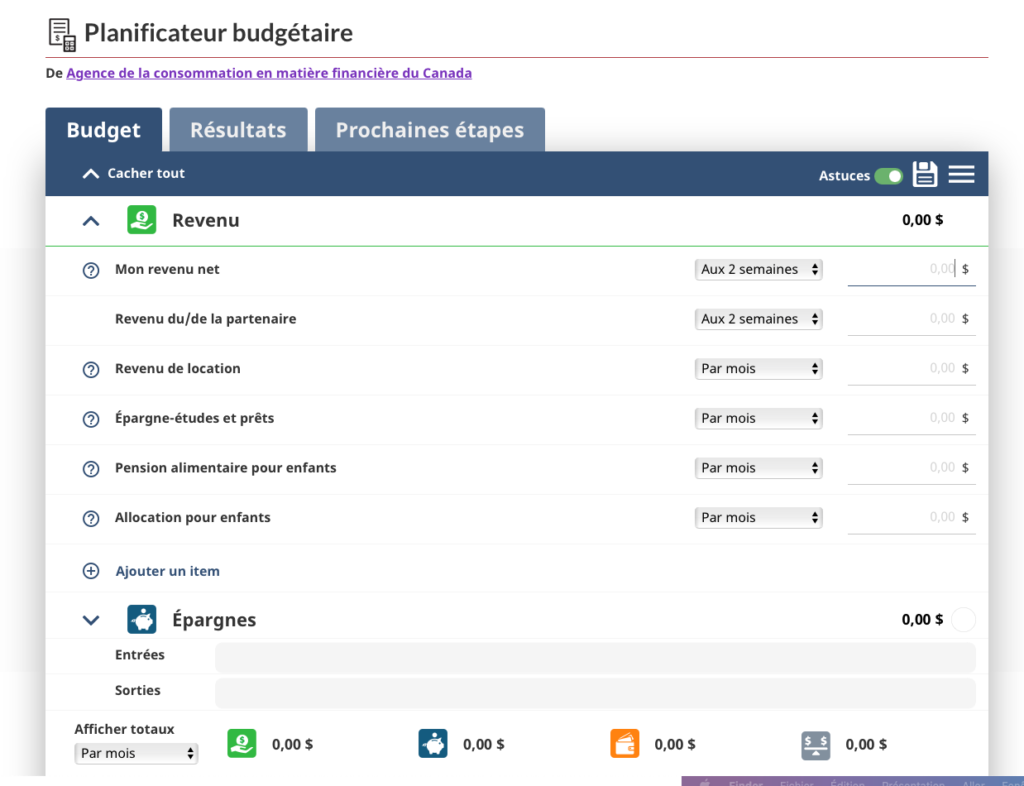

4 - Make a budget

And are there any foolish expenses? There’s another good question! Did you ever ask yourself that? Sometimes we spend it all over the place. But of course my expense is useful, here! For my mood, anyway!

To have control over our wallet, there is nothing better than putting everything in order and drawing up a budget, as Beatrice, Jean-Sébastien and Youcef remind us! We realize the cash outflow that could have been avoided, the superfluous or unforeseen expenses. Each of them has tools to help you.

I can even suggest another one, the one offered by the Financial Consumer Agency of Canada on the Government of Canada site, which is very easy to use.

Beatrice devotes 15 minutes a week to it, Jean-Sébastien does it monthly, it’s up to you to find what suits you.

And what is the “Happiness” budget? Our authors remind us that happiness is not found in money, even if it contributes to it. The idea is not to stop eliminating all non-essential expenses in order to save, since it is still important to enjoy yourself from time to time (like when you travel)!

When analyzing your expenses, ask yourself if you need the latest iPhone, a new computer or cable with all the TV channels? Would you rather go to a restaurant? Or to buy your morning coffee at your favourite convenience store? Is this an expense that could be cut in part?

Being happy doesn’t always require spending money. Knowing what your plans are, what your dreams are, is important! Ask yourself questions to find out what really makes you happy and plan your “Happiness” budget!

5 - Track your credit report

When we start in the workforce, our credit report gets built and our credit score goes up with it. It’s important to know what makes it fluctuate and how to keep it healthy. Why? Because someday you may need to borrow money or apply to a credit card and it could be declined. To do this, check with Equifax and TransUnion!

Finally, keeping track of your file can protect you from identity theft. And that can affect anyone. Equifax reported in November 2020 that fraudsters and thieves were more active since the COVID-19 crisis due to the more intensive use of internet transactions in part.

To prevent these incidents and improve your credit score, take these precautionary measures suggested by Equifax:

- Keep track of your credit card statements as soon as you receive them (or during the month on your online account).

- Regularly request to receive your credit report (this does not affect your score)

- Avoid using Public Wi-Fi networks to track your records

- Regularly update your passwords to ensure they are strong

6 - Stay informed about finances

With the tools that exist now and the ones I’ve suggested above, there are no more excuses for not being financially savvy in 2021!

Read the news, ask Youcef’s group for news and tips, compare bank accounts and credit cards with milesopedia.

Continue to educate yourself on a regular basis to make informed decisions and avoid mistakes!

Conclusion

The objective? Maintaining a healthy connection with money and what source of happiness you’re aiming for.

Finally, as a couple, have an open discussion about money. How much do we earn, how much do we spend, do we have a sufficient pension fund? It’s important for every adult to have a clear vision of his or her financial future.

You have children? Financial education can start very early as long as we don’t go into details so as not to stress them with our financial problems if there are any. Children need to feel financially secure with their parents. It’s up to you to find the right age-appropriate balance to educate them. This can be with pocket money, games, but also books!

Introducing them to money early can lead them to financial stability, but also to the path of entrepreneurship and financial independence!